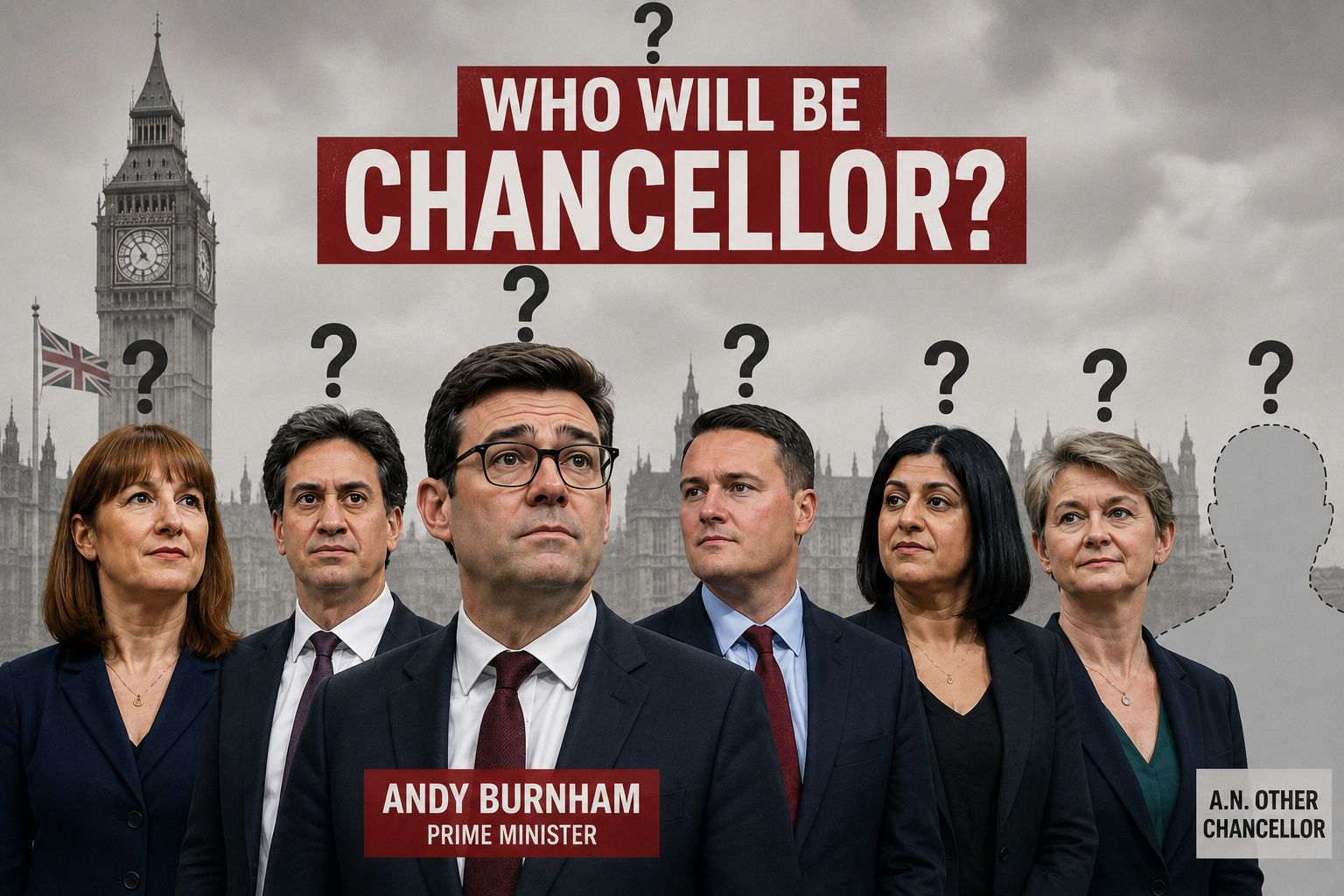

Britain is about to get a new Prime Minister. Andy Burnham, the sole declared candidate for Labour leader, could be in Downing Street by 17 July. Rachel Reeves is reportedly not being retained as Chancellor. And the person Burnham appoints to Number 11 will do more to shape Norfolk’s premium property market than any planning reform or stamp duty tweak.

This is not political commentary. It is financial reality. The Chancellor’s credibility with bond markets directly determines your mortgage rate, your borrowing power, and what your home is worth.

Most homeowners assume their mortgage rate follows the Bank of England base rate. It does not. Fixed-rate mortgages, which account for 85% of UK mortgage products, are priced off swap rates. Swap rates track gilt yields. And gilt yields move on one thing above all else: whether bond traders believe the Chancellor will keep public finances under control.

The chain is short and brutal:

Chancellor credibility → Gilt yields → Swap rates → Mortgage rates → Borrowing power → House prices

When confidence holds, gilt yields stay contained and mortgage pricing remains competitive. When it fractures, yields spike, lenders withdraw products, and buyers lose borrowing capacity overnight.

We saw this in September 2022. Kwasi Kwarteng’s mini-budget proposed £161 billion in unfunded tax cuts. Within a week, 40% of all UK mortgage products were withdrawn. Rates surged above 6%. House prices fell 0.9% in a single month. When Rishi Sunak and Jeremy Hunt replaced Truss and Kwarteng, 30-year gilt yields dropped from over 5% to 3.68%. The market steadied within weeks.

The lesson is simple: the single most important thing a Chancellor does for the housing market is maintain market confidence. Everything else operates in the shadow of that fact.

The Bank of England base rate is 3.75%. But the gilt market tells a harder story.

The gap between the base rate and 10-year gilts is around 135 basis points, the widest in over a decade. This is why fixed mortgage rates have barely fallen despite four base rate cuts in 2025. The best five-year fixes sit around 4.48%. The average is 5.63%.

For Norfolk’s premium market, the numbers are stark. On a £750,000 mortgage over 25 years:

A 1% rate fall saves £430 per month, £5,160 per year, or £25,800 over five years. At £975,000 (a £1.3 million purchase with 25% deposit), that same 1% saves £559 per month or £6,708 per year.

More importantly, lower rates expand the pool of qualified buyers. With lenders applying a 4.5x income multiplier, every reduction in stress-test rates brings more households within reach of a £1 million purchase. That is what drives transaction volumes at the premium end.

Before looking at the candidates, it is essential to understand what Burnham is asking whoever sits at Number 11 to do. The Prime Minister sets the direction. The Chancellor determines whether markets believe it is funded. And Burnham’s agenda is ambitious.

He has called for the most extensive council house building programme since the Second World War: 500,000 social homes by the end of the decade, funded by redirecting the existing £39 billion affordable housing budget entirely towards social rent. He wants to reinstate the northern leg of HS2 at an estimated cost of £36 billion. He has spoken about large-scale retrofit programmes for energy efficiency. He wants to review the employer National Insurance increase introduced by Reeves in the 2024 Budget, which he has called “the wrong decision.” And he wants to reduce water bills, energy costs, and transport fares.

He has also formally backed a land value tax to reform how property and land are taxed in Britain (more on this below).

All of this while committing to maintain the current fiscal rules and not raise income tax, VAT, or National Insurance rates. The tension between ambition and fiscal constraint is the central challenge for whoever becomes Chancellor. And how they resolve it will determine what happens to gilt yields and, by extension, to mortgage rates.

At least nine names are reportedly in the running. Here are the candidates that matter most, and what each would mean for the housing market under Burnham’s direction.

The Energy Secretary is the overwhelming favourite, backed by Labour’s soft left and reportedly “operating under the assumption” that the role is his. He served as a special adviser to Gordon Brown at the Treasury for five years, chaired the Council of Economic Advisers, and has the deepest economic policy background of any contender. He sits on Burnham’s transition team.

The housing case for Miliband. He understands fiscal mechanics at a granular level. Under Brown, he helped shape a period that saw the highest transaction volumes and strongest house price growth of any Chancellor in the last 30 years. He and Burnham have both committed to maintaining the current fiscal rules. His closeness to Burnham means policy coherence between Number 10 and Number 11, reducing the kind of internal friction that unsettles markets.

Burnham’s influence. Miliband is the most ideologically aligned candidate. He would likely embrace Burnham’s social housing programme and retrofit agenda enthusiastically, given his own Net Zero commitments. The risk is that he says yes to everything. If Burnham pushes for HS2, mass social housing, and a retrofit programme simultaneously, Miliband may lack the instinct to push back on timing or scale. The fiscal rules would be maintained on paper, but markets watch spending intentions as closely as spending rules.

The housing case against Miliband. City commentators have briefed hard against his appointment. One prominent analysis warned that “global investors are already very suspicious of Britain” and that Miliband as Chancellor “would be the final sign that the country had become far too risky.” His Net Zero agenda could also impose additional costs on traditional properties through stricter EPC requirements and retrofit obligations. For Norfolk’s stock of period and rural homes, that is a material consideration.

Market signal: Gilt yields likely to tick up 10 to 20 basis points initially as markets test the appointment, then stabilise if fiscal rules are maintained. Net effect on mortgage rates: modest and temporary, provided early actions reinforce discipline.

The Work and Pensions Secretary is described by Westminster insiders as “the ultimate safe pair of hands.” A Blairite who was caught complaining about the scale of welfare spending, he would represent the most fiscally conservative option available to Burnham.

The housing case for McFadden. Bond markets would welcome his appointment. Gilt yields would likely hold or ease slightly. Mortgage pricing would remain stable. For Norfolk’s premium market, stability is valuable in itself because premium buyers are more sensitive to uncertainty than to absolute rate levels.

Burnham’s influence. This is where the dynamic becomes interesting. McFadden would act as a brake on Burnham’s spending ambitions. The 500,000 social homes target would be stretched over a longer timeline. HS2 reinstatement would be delayed or scaled back. The employer NI review would proceed cautiously. Burnham would get fiscal credibility but at the cost of the pace of delivery he has promised. The question is whether Burnham accepts that constraint or whether the resulting tension becomes its own source of market anxiety. History suggests that a PM who publicly overrules a cautious Chancellor does more damage than appointing a spending-friendly one in the first place.

The housing case against McFadden. He has no Treasury experience and would be unlikely to push for bold tax reform. His appointment would not energise any particular housing agenda. A passive Chancellor in an activist government creates drift.

Market signal: Gilt yields stable or slightly lower. The safest option for mortgage pricing in the short term.

The former Health Secretary endorsed Burnham, claimed to have leadership numbers of his own, and is angling for a major role. Some have suggested Chancellor as a way to both reward and contain a potential rival.

The housing case for Streeting. He describes himself as a “progressive capitalist” and is seen as more centrist and pro-business than Miliband. Markets would view his appointment as a moderate signal.

Burnham’s influence. Streeting and Burnham are not natural allies. Streeting endorsed Burnham out of pragmatism, not conviction. As Chancellor, he would likely moderate Burnham’s spending programme, but the relationship would be transactional rather than collaborative. Burnham’s land value tax ambitions would face resistance from a centrist Chancellor wary of alienating property-owning voters. The 500,000 homes programme would be reframed around private sector delivery rather than pure social housing. The risk is the Brown-Blair dynamic: a PM and Chancellor pulling in different directions, creating the kind of uncertainty that bond markets punish.

The housing case against Streeting. No economic policy background. Placing your biggest potential rival next door at Number 11 is historically a recipe for tension.

Market signal: Neutral to mildly positive. Markets would take a “wait and see” approach.

The former Chief Secretary to the Treasury was Rachel Reeves’s deputy and the most vocal defender of fiscal discipline during the leadership transition. He stated publicly that bond markets should be “content” with Burnham’s plans and stressed the importance of not borrowing “indiscriminately.”

The housing case for Jones. Maximum continuity with the current fiscal framework. He understands gilt market constraints at a technical level and has explicitly warned against borrowing promises that cannot be delivered.

Burnham’s influence. Jones has already begun managing expectations around Burnham’s agenda. He has said that “a little bit more borrowing” is feasible within the fiscal rules, but has cautioned that simply announcing “plans to borrow tens of billions” for council housing is “impractical” because “we lack sufficient builders, bricks, and the capacity to connect these projects to the electricity grid.” This is the Chancellor who would say: we can build the homes, but it takes a decade, not five years. Burnham’s LVT would be studied rather than implemented. HS2 would be treated as a long-term aspiration. For mortgage rates, this caution translates to stability.

The housing case against Jones. Unpopular with colleagues. If Burnham overrides his caution, the credibility of the appointment collapses.

Market signal: Gilt yields steady or slightly lower. The “boring but reliable” option.

Shabana Mahmood, the Home Secretary, was many observers’ top pick. Described as the government’s most able minister and “rock-solid reassurance to the City,” she reportedly believes in actually cutting some areas of spending. She has chosen to stay at the Home Office. Under Burnham, she would have been a formidable restraining influence on spending, the kind of Chancellor who would tell a PM “you can have two of those three priorities, not all of them.” Her withdrawal has been a loss for anyone hoping for fiscal discipline with political weight.

Yvette Cooper, the Foreign Secretary, is a former leadership candidate with an experienced backroom team. Rachel Reeves staying on is seen as a last resort by Burnham’s camp. Torsten Bell, the pensions minister and former Resolution Foundation head, is intellectually credible but lacks political standing.

Buried in the leadership contest is a policy that could fundamentally reshape the cost of owning a high-value home.

Burnham has formally backed a land value tax (LVT): an annual levy on the unimproved value of land. He has described it as “a very productive form of taxation” and has suggested using revenues to eliminate stamp duty and reform council tax. UK land was valued at £7.1 trillion by the ONS in 2024. At a hypothetical rate of 0.5%, a levy would raise approximately £35.5 billion per year.

For Norfolk’s premium market, this would be a seismic shift. Currently, the cost of buying is front-loaded through stamp duty (£43,750 on a £1 million main residence). The cost of holding is spread through council tax, which is based on 1991 valuations and is relatively modest even in the highest bands.

Under an LVT or proportional property tax model, stamp duty would be eliminated but replaced with an annual charge based on current values. One campaign group, which has cross-party support including from Burnham, has proposed a rate of 0.48% of property value. On a £1 million home, that is £4,800 per year. On a £2 million home, £9,600.

Transition provisions would likely cap annual increases at around £1,200 per year and offer deferrals for asset-rich, cash-poor homeowners. The cap would lift when a property is sold, since the buyer would have benefited from the removal of stamp duty.

This is not confirmed policy. Burnham has not committed to a specific rate or timeline. But the direction of travel is clear: from a one-off transaction cost to an ongoing holding cost. Which chancellor Burnham appoints will determine how fast this moves from aspiration to reality. Miliband would accelerate it. McFadden or Jones would park it.

Any serious analysis of the medium-term outlook has to address the next general election, due by 2029.

Reform UK has positioned itself as explicitly pro-property. Its stated policies include raising the stamp duty threshold to £750,000, increasing the inheritance tax threshold to £2 million, restoring full mortgage interest relief for landlords by reversing Section 24, and scrapping net zero housing targets.

The stamp duty saving is significant. A buyer at £1 million currently pays £43,750. Under Reform’s proposals, that could fall to around £16,250, a saving of £27,500.

But here is the paradox. Reform’s broader fiscal agenda involves tens of billions in unfunded tax cuts. The Bank of England Governor has publicly stated that their proposed bank tax would raise borrowing costs. Market analysts have warned that a Reform government “would likely compel investors to seek a higher return for the risks associated with backing the UK.”

The arithmetic is unforgiving. A 1% rise in mortgage rates on a £750,000 loan costs the buyer £5,160 per year. The stamp duty saving of £27,500 is wiped out in just over five years. And unlike stamp duty, which is paid once, the higher mortgage cost continues for the life of the loan.

Markets will not wait for an election result. If polling tightens, gilt yields will move, swap rates will follow, and mortgage pricing will shift well before any vote takes place.

Norfolk has 314 properties listed above £1 million, spending an average of 262 days on the market. The premium segment represents 3 to 4% of total stock. It is a market defined by quality, scarcity, and the financial capacity of a small pool of committed buyers.

For the next 12 to 18 months, the decisive variable is not who holds which political title. It is where gilt yields settle and what that means for mortgage pricing.

If the incoming Chancellor reassures bond markets, gilt yields could gradually ease, and five-year fixed rates might drift towards the low 4% range. That would meaningfully support premium transaction volumes.

If the transition introduces uncertainty, gilt yields will stay elevated or rise. Mortgage rates above 5% would become entrenched, extending days on market and increasing price sensitivity.

The fundamental dynamic has not changed. Norfolk’s premium segment moves on quality of stock, desirability of location, and the financial capacity of buyers. What changes is the cost of the capital those buyers use to transact. And that cost is set not in Westminster, but in the gilt market, which is watching Westminster very carefully indeed.

We track these macro trends precisely because they determine pricing outcomes for every property we bring to market. Understanding what drives your market is how we price accurately and sell effectively.